Query? We are “forming” a Hindu Undivided Family (HuF). What is the Date of Formation in case of HuF for the purpose of PAN Application in Form 49A.

Response: Hindu Undivided Family or Joint Hindu Family is a creature of Hindu Law. It is not “formed” by Agreement as in case of a Partnership or incorporated under a statute as in case of a Company. It exists by fact qua the coparceners inter-vivos.

1. So once the coparcenary is created i.e., by Birth of an offspring (Male or Female), that is the day the HuF is Formed.

2. In case of property allotted on Total Partition of a Bigger (Parent) HuF to a Male, the same retains the character of coparcenary / HuF property and in case the allotee is an unmarried Male (or Minor) – the Date of Marriage would be the Date of Formation of His HuF.

3. The Affidavit accompanying Form 49A – application for Allottment of PAN to HuF – also referred to a HuF deed – is merely an affirmation of facts with respect to Members, Karta & Date of Formation as above.

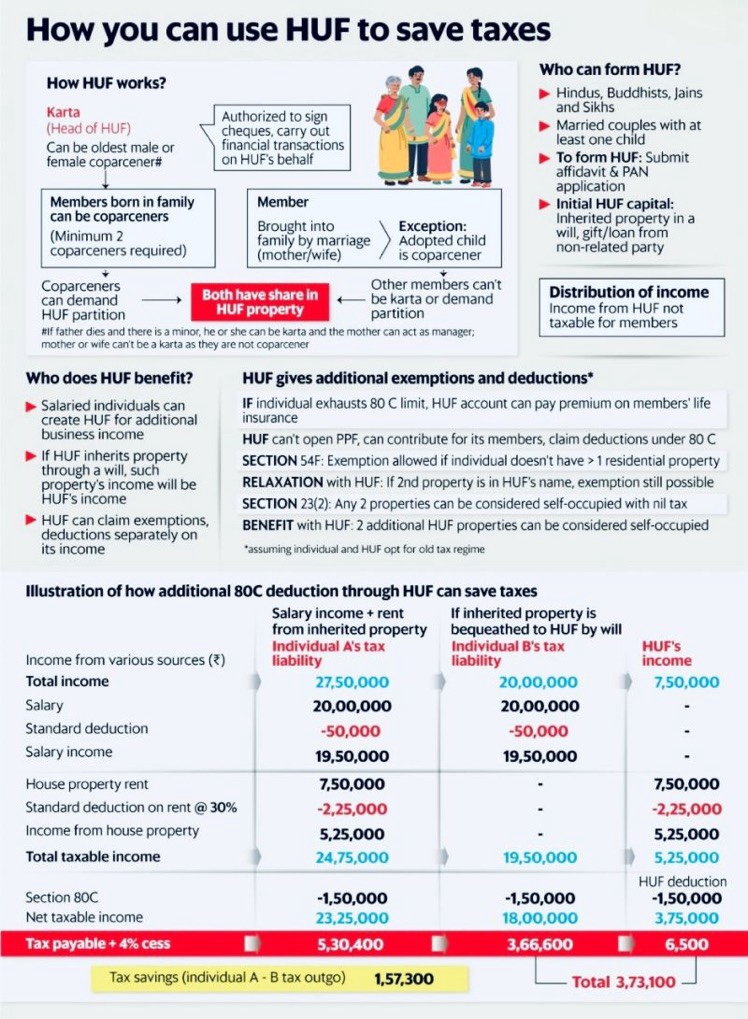

What is colloquially referred to as the “creation” or “formation” of HuF is actually the creation of HuF File for Tax / Banking / Civil Law purposes with Introduction of Capital.

Introduction of Capital in case of HuF

1. Gifts From Stranger

It is now trite that HuF can receive Gift from Strangers. However, Section 56(2)(x) – Income without Consideration (or Gift) is applicable in case HuF receives the same except from person otherwise as Karta / Members of the HuF.

The gifted property will be HUF property if the gift is made to HUF. Intention of donor & the character of the gifted property will depend on the construction of the gift deed. Several courts have opined from time to time that the “intention” to gift to an HUF and not to any individual has to be explicitly clear.

Clear declaration of intention through affidavit. {C.N. Arunachala Mudaliar Vs C.A. Muruganatha Mudaliar & Anr. AIR 1953 SC 495: (1954) SCR 243 (SC)}

No specific bar to a gift by the father to the HUF of his son, his wife & minor children. However, for avoiding the clutches of sec 64 (1)(vi) such gifts better be avoided. {CIT Vs Smt. T. Suryamani Kothavalasala (2003) 263 ITR 271 also see CIT Vs S.N. Malhotra (1989) 178 ITR 380 (Cal)}

2. Gifts from Members of the HuF– Implications thereof

Gift received by HuF from Karta or Members of the Family is also referred to as Blending of Individual Property with the Family Hotchpot. The same attracts Clubbing of Income u/s 64(2) of the Income Tax Act, 1961 and the same is deemed to be the income of the Transferor Individual.

3. Inheritance by a HuF / Specific Bequest to HuF under a will.

A bequest of money/property to an HUF can also be done by a Will provided the Will clearly states that the bequest is in favour of the HUF.

4. Property allotted on Partition of Parent (Bigger) HuF

Property received on Total Partition (recognised u/s 171 of the Income Tax Act, 1961) of a Bigger (Parent) HuF by a coparcener having a family, continues to have the characteristic of coparcenary / HuF property.

An unmarried coparcener receiving any property will own the property in the status of HUF until he acquires the status of HUF. In case of married coparceners who have no child, the property will continue with the status of HUF as held by High Court of Madhya Pradesh in CIT vs. Krishna Kumar (1982) 10 Taxman 292 (MP).

5. Accumulation of Income from Joint Family Property

Property acquired in the course of some business carried on by the persons constituting a joint Hindu family, takes the characteristic of joint family property.

Further, accumulation of income earned from Joint Family Property retains the character of HuF property until the same is Allotted to Members on Total Partition.