Download This Document in PDF – Operating Leverage A New Dimension

This paper is also available on the SSRN online library (Link outside web-blog).

Abstract

Hitherto, in determining Operating Leverage, it is assumed that selling price does not vary with changing price of goods, thus inherently violating the Law of Demand. This paper presents the sensitivity of Operating profits to simultaneous change in selling price and quantity of goods sold and formulates functions referred to as Price Leverage – which serves as a measure for the impact of changes in selling price on the operating profit and Total Operating Leverage – which serves as a measure for the combined impact of simultaneous change in selling price and quantity of goods sold. Further, the paper presents the application of concepts of Price Elasticity of Demand to sensitivity of operating profits, for determination of Break-even Point (BEP) and Optimum Capacity Utilization (or the level of Profit Maximization).

1. Introduction

Sensitivity Analysis, that is, the impact of change in one or more independent variables, on the dependent variable, forms the basis of management decisions ranging from project appraisal to determination of selling price or production quantity. It is defined as the study of how the uncertainty in the output of a mathematical model or system (numerical or otherwise) can be apportioned to different sources of uncertainty in its inputs.1

Leverage (also referred to as Gearing in United Kingdom and Australia) is a general term for any technique to multiply gains and losses2. Operating Leverage is one of the popular methods to ascertain the firms operating risks and its impact on operating profits or earnings. A firm’s operating leverage involves a choice among alternative production arrangements which differ in terms of “fixed” and “variable” cost component3.

Degree of Operating Leverage can be computed by a number of equivalent ways, including:-

where

In all studies of Operating Leverage, hitherto, it is assumed that the selling price does not vary with changes in quantity of goods sold, thus, inherently violating the Law of Demand, that is, ceteris paribus, selling price and quantity sold are inversely proportional to each other and as price increases, quantity decreases and vice versa5, the notable exceptions of this Law being Veblen Goods (conspicuous consumption) and Giffen goods (inferior goods).

Price Elasticity of Demand measures the responsiveness of the quantity of good or service demanded to changes in its price. It is measured as the ratio of % change in quantity to % change in price.

The Co-efficient of Price Elasticity of Demand tends to be negative

due to the inverse nature of the relationship between price and quantity demanded, as described by the “law of demand”5.

2. Sensitivity of Operating Profits to changes in Selling Price.

Sales are a function of selling price and quantity of goods sold.

Variable costs can be categorized as:-

-

costs directly proportional to Selling price such as Indirect Taxes and Selling expenses;

-

costs directly proportional to Quantity such as production & distribution costs.

For ease of calculations, we can determine the Net Realisable Value as Selling Price less Variable Costs proportional to Selling Price.

Therefore,

Now, the revised format for Computation of EBIT will be as under

| Sl# |

Particulars |

Symbols |

per unit |

Amount |

| 1 |

Quantity (units) |

q |

||

| 2 |

Selling price |

s |

||

| 3 |

Less: Variable Costs (proportional to Selling Price) |

VCsp |

||

| 4 |

Net Realisable Value [(2)-(3)] |

NRV |

||

| 5 |

Less: Variable Costs (proportional to Quantity) |

VCq |

||

| 6 |

Contribution [(4)-(5)] |

C |

||

| 7 |

Less: Fixed Costs |

FC |

||

| 8 |

Operating profit or EBIT [(6)-(7)] |

EBIT |

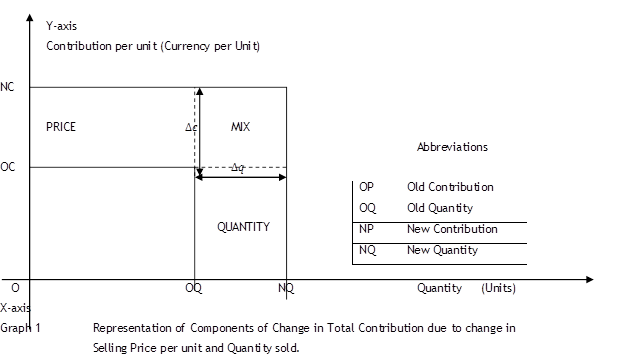

The Contribution is affected by changes in

-

Selling Price ;

-

Quantity sold ; and

-

Variable costs.

Accordingly, there are three components of Changes in Operating Income due to change in Selling Price or change in Quantity of Goods Sold:-

-

Price Leverage which factors in Selling Price and the Variable Costs proportional to Selling Price.

-

Quantity Leverage or Operating Leverage which factors in Quantity of Goods Sold and Variable Costs proportional to Quantity and Fixed Costs.

-

Mix Leverage which factors in the simultaneous change in Price and Quantity.

Price Leverage measures the sensitivity of operating profits to changes in Net Realisable Value. It computed as the ratio of Net Realisable Value (or Sales less Variable Costs proportional to Selling Price) to operating profits (EBIT).

Where

Mix Leverage (or Mix of Quantity & Price Leverage) measures the sensitivity of operating profits to simultaneous change in Quantity and Price. It is computed as the product of Degree of Price Leverage and % Change in Net Realisable Value and % Change in Quantity.

Where

∆q = Change in Quantity ; q = Original quantity

∆p = Change in Net Realisable Value ; p = Original Net Realisable Value

Total Operating Leverage measures the sensitivity of operating profits to simultaneous change in Quantity and Price. It is computed as under

Total Operating Leverage can also be computed as function of Price Elasticity of Demand (η)

3. Determination of Break Even Point (BEP)

The operating break-even point is the level at which operating profits are NIL.

This can be possible for a point where Total Leverage = 0

Solving this, we get a quadratic equation, as

We know, that the root of a quadratic equation are :

where

Note: For computing BEP (quantity), use corresponding signs while determining BEP (price).

4. Determination of Optimum Capacity Utilization (for maximum profit)

Simply stated, optimization is the selection of a best element (with regard to some criteria) from some set of available alternatives6. In the context of a firm’s operations, optimum capacity utilization is basically the determination of the level of production at which operating profits are maximum, the level after which operating profits start diminishing.

… (1)

… (1)

Differentiating equation (1) we get;

Further differentiating equation (2) we get;

As we know that according to law of demand, for all goods other than Veblen goods and Giffen goods, the price elasticity of demand (η) is less than zero (and hence negative).

Accordingly, f”(x)<0,for all goods other than Veblen and Giffen goods, and we can get the point of maximum profits by equating f'(x)=0

Solving this we get;

5. References

-

Saltelli, A., Ratto, M., Andres, T., Campolongo, F., Cariboni, J., Gatelli, D. Saisana, M., and Tarantola, S., 2008, Global Sensitivity Analysis. The Primer, John Wiley & Sons.

-

Brigham, Eugene F., Fundamentals of Financial Management (1995).

-

Uncertainty, the Theory of Production and Optimal operating leverage, by Ronald E. Shrieves, Southern Economic Journal, Vol. 47, No. 3, Jan., 1981

-

Png, Ivan (1989). p.57.

-

Gillespie, Andrew (2007). p.43.

- “The Nature of Mathematical Programming,” Mathematical Programming Glossary, INFORMS Computing Society.

(c) CA. Nirmal Ghorawat and CA. Ronak Shah

The Authors are the members of the ICAI.