Financial Transaction are Diagonally Opposite and Equal* for Counter-parties to a Transaction

This hold’s special significance when we consider a Scenario where the Accounting Package sends and receives these Financial Transaction Vouchers and also intelligently deciphers / decodes these Financial Transaction Vouchers to be put to meaningful use without manual extraction or re-keying. [See my other post XBRL : GL in International Trade Transactions]

* The Equality yard-stick, may in, certain cases be distorted, by differences on account of RECOGNITION (across different periods, Capital or Revenue) or MEASUREMENT (fair value, historical cost, etc) of Financial Transactions.

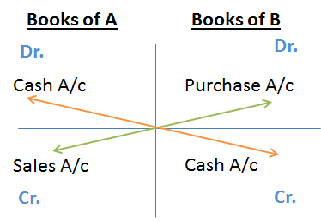

Eg. A Sells goods to B for CU X, on cash payment.

Recording of Transaction

In books of A

Sales Cr, Cash A/c Dr, Amt – CU X

In books of B

Cash A/c Cr, Purchase A/c Dr, Amt – CU X

| Principal Party (A) | Counter-Party (B) |

| SALE/INCOME | PURCHASE/EXPENSE |

| RECEIPT | PAYMENT |

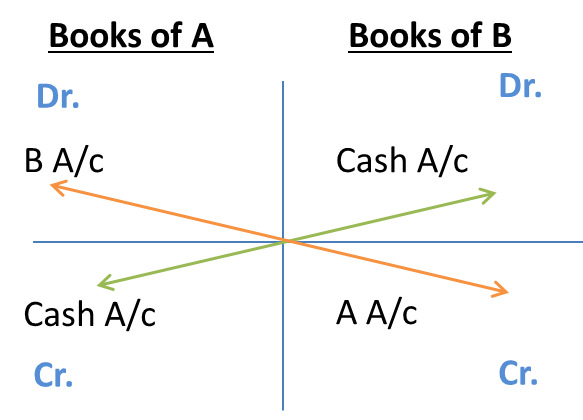

Eg. B pays CU X to A

Recording of Transaction

In books of A

B A/c Cr, Cash A/c Dr, Amt – CU X

In books of B

Cash A/c Cr, A A/c Dr, Amt – CU X

| Principal Party (A) | Counter-Party (B) |

| RECEIPT | PAYMENT |

| DEBT DUE TO B(A IS DEBTOR OF B) | DEBT DUE FROM A(B IS CREDITOR OF A) |

3 responses to “An Observation in Book-Keeping”

[…] An Observation in Book-keeping […]

I was asked to provide some links to the references provided:

EDIFICAS demonstrated the mirrored customer/vendor process on page 27 in its document that is available here: http://www.edificas.fr/content/download/216/1169/version/1/file/TIC-CR+1.8+Fran%C3%A7ais.pdf – Google says it is from 2006, but that is impossible, as XML didn’t become a recommendation until 1998 and it mentions XBRL; and EDIFICAS didn’t collaborate with the XBRL community until the early 2000s. EDIFICAS, based in France, has helped lead the development of UN/CEFACT accounting standards for decades.

Bill McCarthy’s REA model is well documented and his work for ebXML,especially around the CPA (not certified public accountant, but collaboration protocol agreement) are largely based on the mirrored model. See https://www.msu.edu/user/mccarth4/DUNN&MC.htm – Bill, a Michigan State University professor and accounting thought leader, is sometimes referred to as the Father of ERP.

There was a link to Todd’s materials in the prior message; a visit to archives of GLDialTone.com when he owned it (e.g., https://web.archive.org/web/20000302080601/http://www.gldialtone.com/) reveals some amazingly creative thought in the space; he was prolific and thought provoking, whether you agreed or not and without question controversial. The current URL is no longer filled with his content, which is why you need to use cached copies like those in the Wayback machine. Todd’s passions are currently directed at stopping war and opposing the military and imperialism, if I am correct.

There are only so many islands of thought in this ERP audit data standardization space, led by EDIFICAS, Bill, the SIE group in Sweden, the Auditfile group in the Netherlands – which seeded the OECD SAF-T group, and the XBRL GL group – these are chief amongst them, as I see it.

You note both “Financial Transaction are Diagonally Opposite and Equal* for Counter-parties to a Transaction” and that there are issues/distortions – recognition, measurement.

The “mirror” of acconting transactions to counterparties: the concept of potentially being able to remove accounting from organizational manipulation and conduct them according to agreed-upon events independently in third party/netledgers using mirrored events is common to the writings of EDIFICAS, Bill McCarthy and Todd Boyle, amongst others (as recently noted at http://financialcryptography.com/mt/archives/001469.html). That author likens the current Bitcoin model as reflective of that school of thought. The US Government has a USSGL which publishes standard accounts and transaction sets for a broad range of pre-determined events.

While it is helpful to think in generalities that one company’s accounts receivable is another’s accounts payable, or one group’s “due to” is another’s “due from”, there are some important issues to remember, as you point out:

In some environments, organizations are permitted or required to have different accounting methods. A small company may be on a cash basis, where a larger one may be accrual, a not-for-profit on a different method and a government a different one yet. Accounts receivable reflected on the accrual basis seller may not be reflected on the cash basis buyer until the money changes hands. A sale on one organization’s books may be a purchase or a lease on another’s books. And a transaction for US GAAP for a US domestic company of foreign private issuer may be recorded differently for an IFRS filer – capitalized in one, expensed in another.

Likewise, the imposition of an intermediary changes things once again. In particular, an independent agent may receive insurance premiums from a policy holder, but the accounting is now a three way match in different combinations.