Section 2(9) of the Benami Transactions (Prohibition) Act, 1988 defines the scope of a “transaction” or “arrangement” labelled by Law as “Benami”.

(A) a transaction or an arrangement :-

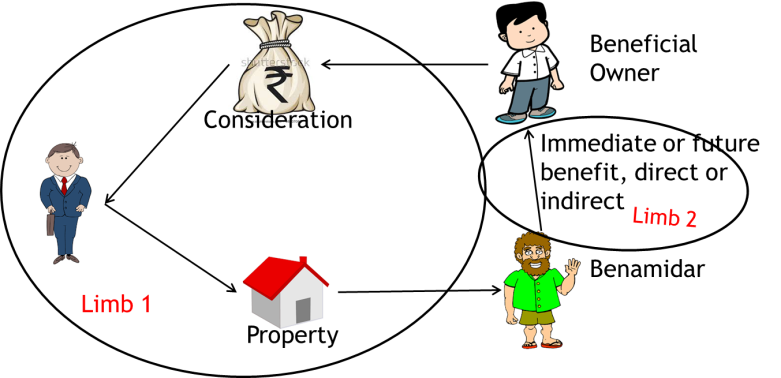

(a) where a property is transferred to, or is held by, a person, and the consideration for such property has been provided, or paid by, another person; and

(b) the property is held for the immediate or future benefit, direct or indirect, of the person who has provided the consideration.

except when the property is held by –

(i) a Karta, or a member of a Hindu undivided family, as the case may be, and the property is held for his benefit or benefit of other members in the family and the consideration for such property has been paid or provided out of the known sources of the Hindu undivided family;

(ii) a person standing in a fiduciary capacity for the benefit of another person towards whom he stands in such capacity and includes a trustee, executor, partner, director of a company, a depository or a participant as an agent of a depository under the Depositories Act, 1996, and any other person as may be notified by the Central Government for this purpose;

(iii) any person being an individual in the name of his spouse or in the name of any child of such individual and the consideration for such property has been paid or provided out of the known sources of the individual;

(iv) any person in the name of his brother or sister or lineal ascendant or descendant, where the names of brother or sister or lineal ascendant or descendant and the individual appear as joint owners in any document, and the consideration for such property has been paid or provided out of the known sources of the individual; or

(B) a transaction or an arrangement in respect of a property carried out or made in a fictitious name.

(C) a transaction or an arrangement in respect of a property where the owner of the property is not aware of, or, denies knowledge of such ownership

(D) a transaction or an arrangement in respect of property where the person providing the consideration is not traceable or is fictitious.

Explanation.- For the removal of doubts, it is hereby declared that benami transaction shall not include any transaction involving the allowing of possession of any property to be taken or retained in part performance of a contract referred to in section 53A of the Transfer of Property Act, 1882, if, under any law for the time being in force –

(i) consideration for such property has been provided by the person to whom possession of property has been allowed but the person who has granted possession thereof continues to hold ownership of property;

(ii) stamp duty on such transaction or arrangement has been paid; and

(iii) the contract has been registered.

Section 2(9)(A) of The Benami Transactions (Prohibition) Act, 1988

| 1 | “A” acquires a property in the name of spouse or child and out of the known sources of income of “A” | Not a Benami Transaction |

| 2 | “A” acquires a property in the name of spouse or child but out of “undisclosed income” of “A” | Benami Transaction |

| 3 | “A” acquires a property in the name of brother or sister or any lineal ascendant or descendant and the property is held in joint name and out of the known sources of income of “A” | Not a Benami Transaction |

| 4 | “A” acquires a property in the name of brother or sister or any lineal ascendant or descendant and the property is NOT held in joint name and out of the known sources of income of “A” | Benami Transaction |

| 5 | “A” acquires a property in the name of brother or sister or any lineal ascendant or descendant and the property is held in joint name but out of “undisclosed income” of “A” | Benami Transaction |

| 6 | “A” acquires property in the name of “B” – a person “Benami” (not spouse / child / brother / sister / lineal ascendant or descendant) | Benami Transaction |

| 7 | “A” acquires property in the name of “B” & “B” is not aware of or denies any knowledge of such ownership. | Benami Transaction |

| 8 | “A” acquires property in the name of “B”. “B” does not exist or is a “fictitious” person / entity. | Benami Transaction |

| 9 | “A” acquires Immoveable property (Possession under Part Performance u/s 53A of Transfer of Property Act, 1882) in his own name. However, the Title Deeds are not registered in the name of “A” and the “Possession Deed / Power of Attorney / Agreement of Sale” are not registered and / or Stamp Duty is not paid on the transaction. | Benami Transaction |

| 10 | “A” acquires Immoveable property (Possession under Part Performance u/s 53A of Transfer of Property Act, 1882) in his own name. However, the Title Deeds are not registered in the name of “A” but the “Possession Deed / Power of Attorney / Agreement of Sale” IS registered and Stamp Duty IS paid on the transaction. | Not a Benami Transaction |

| 11 | “B & Sons (HUF)” acquires Property in the name of Karta and / or Coparceners or Members of the HUF | Not a Benami Transaction |

| 12 | A & B – a Partnership Firm acquires Property in the name of its Partner A or Partner B | Not a Benami Transaction |

| 13 | DEF Private Limited – a Limited Company acquires Property in the name of its Director – K | Not a Benami Transaction |

| 14 | Help Trust – an AOP (Trust) acquires Property in the name of its Trustee – L | Not a Benami Transaction |

| 15 | Z holds title of property. However, the consideration has been provided by one “U” and “U” is not traceable / fictitious. | Benami Transaction |

| 16 | D transfer his property to S (his spouse / child / lineal ascendant or descendant) to avoid his lawful debts / Creditors | Benami Transaction |

2 responses to “Benami Transaction Examples”

[…] Benami Transaction Examples […]

[…] Benami Transaction Examples […]